TLDR — Treasury’s recent update

- IRS Notice 2025-42 has been released (IRS). For projects that did not begin construction under prior rules before September 2, 2025:

- If the solar project is >1.5 MW AC, you can no longer lock incentives by spending 5% up front; you now need real construction work to “begin construction.”

- If the solar project is ≤ 1.5 MW AC, you can still use the 5% path to qualify for the ITC.

- Battery projects are unaffected by the new treasury guidance.

- Finish-by dates (the “4-year continuity safe harbor”): if you begin in 2025, finish by 12/31/2029; if you begin 1/1/26–7/4/26, finish by 12/31/2030. (Holland & Knight)

🔥 Exec Summary:

Federal tax credits for solar, energy storage, and other technologies are changing. A new law signed on 7/4/25 (One Big Beautiful Bill (OBBB)) will soon remove the 30%+ federal investment tax credits (ITC) on solar. Yet it largely maintains the 30% credit value for energy storage. The rules are complex, and critical implementation details were just clarified by IRS Notice 2025-42. (IRS)

The bottom line is that for solar projects, there’s now an industry sprint underway to move from concepts to contracts, and lock in terms under current incentive structures.

What this means for commercial landlords & tenants: there is an open but limited window to lock in a no-cost “call option” on ITC-supported solar projects. To give projects the best chance of benefiting from today's tax credits, and avoiding the potentially onerous foreign materials requirements, we advise that feasibility and procurement commence ASAP, so that contracts can be signed in 2H’25.

What happened: tax credit changes in the OBBB

OBBB shrinks the ITC window for rooftop solar. The One Big Beautiful Bill (signed July 4, 2025) ends the technology-neutral 30% Section 48E ITC for solar projects placed in service after December 31, 2027.

More detail:

- The Section 48E ITC for solar (30% base federal tax credit to the system owner) will be fully phased out for projects that are signed, developed, constructed and finally Placed in Service (PIS) after December 31, 2027, except for projects that begin construction within 12 months of enactment of the OBBB. (IRS)

- Projects that begin construction within 12 months of enactment of the OBBB (i.e., by 7/4/2026) are allowed Placed in Service (PIS) dates in 2028, 2029, and 2030 (via the four-calendar-year continuity safe harbor). (Holland & Knight)

- However, all projects that do not begin construction by December 31, 2025 are subject to the material assistance from prohibited foreign entities rules (FEOC), the full impacts of which are still being analyzed by the industry. Notice 2025-42 did not address FEOC Beginning of Construction (BOC) rules; Treasury says separate guidance is coming. (IRS)

Escape hatch: “commence construction” by 7/4/26

The one escape hatch is to commence construction no later than July 4, 2026; these projects get until the end of 2029–30 to finish, but anything starting after the cutoff loses the credit. Treasury has now specified how “begin construction” works post-OBBB:

- For solar ≤ 1.5 MW (AC): you may still use the 5% cost safe harbor or the physical-work path to establish BOC before 7/4/26. (IRS)

- For solar > 1.5 MW (AC) and for wind: the 5% safe harbor is no longer available under the new notice; you must rely on the physical work test (on-site work of a significant nature or qualifying off-site custom work under a binding contract, not from inventory) and maintain a continuous program of construction. (IRS)

How to “commence construction” today.

Developers will generally make these undertakings once they have clear commitment from the customer in the form of a signed lease, PPA, or similarly binding agreement.

Practical takeaway for solar projects: act now

If you want the 30% ITC on a rooftop solar project: move quickly—conduct feasibility, get bids, and complete contracting so that your chosen Developer can (a) kick off physical work (e.g., racking foundations, conduit, service upgrades) or(b) for ≤ 1.5 MW AC sites, place qualified equipment orders totaling ≥ 5% of the all-in budget under binding contracts—before the relevant deadlines—and then hit the finish-by dates (2029/2030, depending on when you begin). (Holland & Knight)

Get a free evaluation for any property from Lumen Energy here.

Batteries largely retain access to tax credits, yet with greater requirements for domestic content

- Battery ITC largely preserved. The accelerated phase-out OBBB imposed on wind and solar does not apply to energy storage technology—including storage installed alongside a wind or solar facility.

- Credit value framework unchanged: base 6% / 30% with labor rules; adders still stack. Under Section 48E, storage continues to earn a 6% base credit that steps up to 30% when prevailing wage & apprenticeship (PWA) requirements are met; domestic-content and energy-community bonus amounts remain available, allowing effective rates materially above 30% when stacked.

- Commencement-of-construction interplay when paired with solar. Because the harsh new deadlines target wind and solar, a co-located project can, in principle, have its storage portion qualify under the longer battery schedule even if the solar portion misses the wind/solar deadlines, provided the battery meets the 48E rules on its own (cost allocation, separate interconnection or functional independence often used in practice—confirm with tax counsel). (Notice 2025-42 focuses on wind/solar BOC; storage wasn’t the target of this notice.) (IRS)

- Foreign-sourced supply chain limits now bite batteries too. OBBB layers in new Prohibited / Specified Foreign Entity rules across Section 48E technologies, including storage (separate Treasury guidance forthcoming). (The White House)

Will solar pencil in a post-OBBB world?

Yes. but differently.

All else equal - reducing solar tax credit cuts solar IRRs, and reduces solar lease rates that Developers can pay Landlords.

But other factors are not equal. Over the next 12-24 months, the loss of solar tax credit will be offset against these mitigating factors:

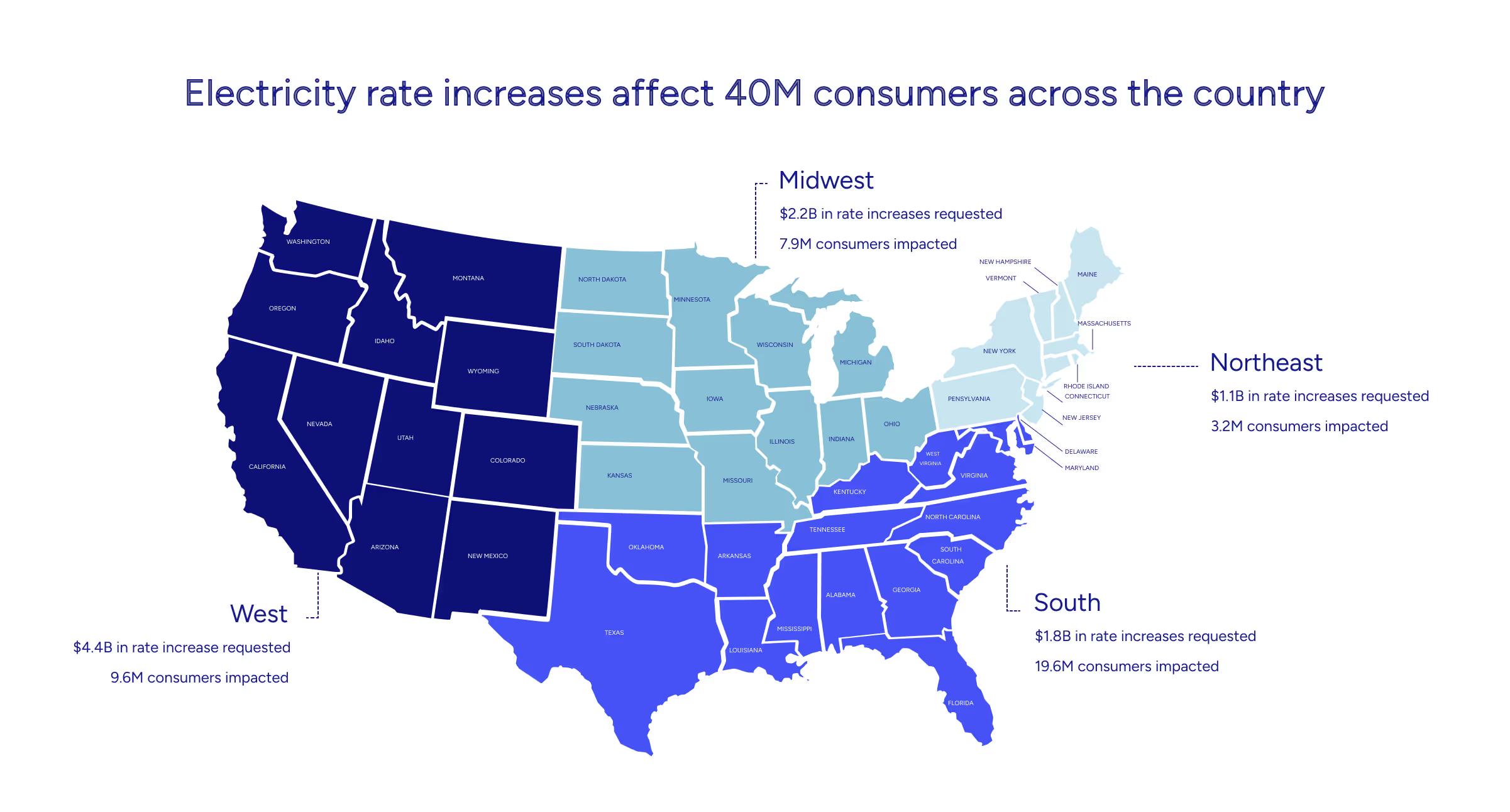

- Rising electricity prices. Utilities have already requested $29 billion in rate increases for just the first half of this year, hitting 40 million Americans. Already-rising retail electricity prices will now get pushed higher, which will both support higher rooftop lease and PPA rates.

- Expanding state policies. These rising prices are pushing local governments to seek relief by incentivizing local power. New Jersey just enacted an additional 3,000 MW of community solar, directing BPU to open registrations by Oct 1, 2025 and accept applications through Dec 31, 2029 (or until capacity fills)—a tailwind for CRE rooftops. (NJ.gov, pv magazine USA)

- Lower financing costs. Removing tax equity layers can reduce cost of capital for some structures.

- Batteries can hybridize with solar. Federal tax credits remain for batteries into the 2030s; utilities are demanding more capacity as costs fall.

Lumen is already supporting many of the largest institutional real estate owners to smartly advance their solar strategies. Lumen's data platform runs live financial models against thousands of commercial properties to determine the highest $NPV option across multiple financing types to support any ownership strategy.